Why bank credit is the predictor of home prices, not interest rates

Money is cheap these days in advanced economies, and I mean really cheap. Unlike 20 or 30 years ago, you can now get a real interest rate of 2 to 4 percent on pretty much any big ticket item. Homes are being financed for these kinds of rates, businesses are tapping into loans at these prices, and consumers are often able to finance a brand new car purchase at zero percent, that's even lower! Unsecured personal lines of credit can hover around 5 percent.

Even though interest rates for companies and consumers are basically hovering closer to zero than at any previous moment in time, there's confused as to why our economies are experiencing weak growth. Lowering interest rates is supposed "spur" economic growth, according to economists, pundits, and economic textbooks. Current logic dictates that cheaper money encourages people to spend more on goods and services, invest in productive business (because you're not going to get much of a return holding your money in a bank account), and help those with high debt-to-income ratios with their spending.

The gap between the logic and reality is big. Borrowing money for a car costs nothing these days, but car sales have been declining since 2013. Gross domestic product (GDP) in all advanced economies is coming in quite shy of historical performance, when double digit economic growth coincided with double digit interest rates. In Europe, rates have gone negative, but European economic growth continues to contract. Folks are now saying that the latest round of interest rate cuts in the US are not spurring growth in the US housing market.

The weird situation in the Canadian housing market

The situation is even weirder in Canada, where low rates over the last two years have not helped a consolidating housing market. So, what the heck is going on? Shouldn't lower interest rates help more people buy a home and boost prices?

Home prices in Canada have been contracting, as measured by Statistic Canada's new home price index. This is the first time home price growth has entered negative territory since late 2009. See the chart below:

Home prices are now contracting, but interest rates remain historically-low. In fact, based on the chart above, housing price growth almost seems correlated with interest rates (you can see growth going down as interest rates trend down between 2009 and 2016). Admittedly, this is a head-scratching situation for any housing analysts, and maybe even for folks who are just trying to figure out if they should buy a home.

But, wait, what's that gray shaded data that looks like mountainous terrain on the chart? That's residential bank mortgage growth. More bank mortgage growth means more bank money has been lent out for the purpose of purchasing a home. Over time this growth has exploded, and so now we've ended up with a massive dollar figure. Total outstanding bank mortgage credit across Canada is now measured in the trillions! As it stands, about 1/3 of all bank credit issued in Canada has gone toward home purchases.

What's interesting is that Canadian housing prices have typically grown in lockstep with residential bank mortgages. In fact, from the chart above we can see that home price growth is correlated with bank mortgages, much more so than with interest rates.

How interest rates are poorly correlated with home prices

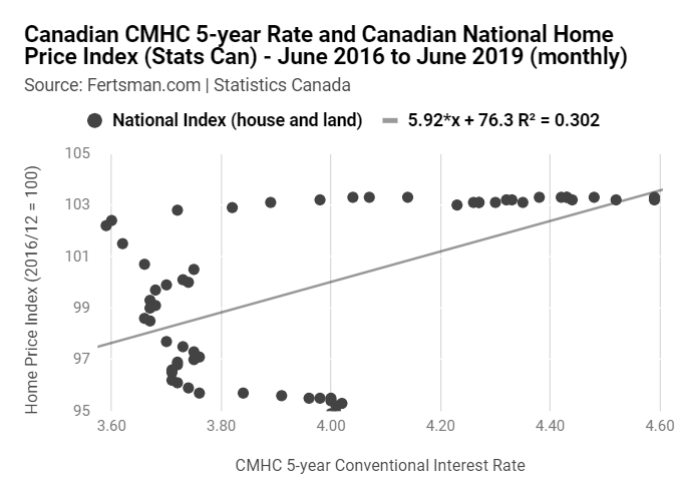

The correlation between home prices and interest rates is quite awful. And if you're working for a company or organization trying to figure out where things are heading based on the cost of credit, you'll likely end up with no answer.

Drawing on CMHC's 5-year conventional mortgage rate and Statistics Canada's home price index for the last 3 years, the relationship between interest rates and home prices is nonexistent in the data. Using a scatter plot chart, we see that there's an r-squared value of 0.302, which indicates little to no relationship between the two variables. The line running through the chart is also not representative of what conventional thinking tells us about interest rates and home prices. The line is supposed to run downward if higher interest rates mean lower home prices. Instead, the line of "best fit" seems to be telling us that there's a positive correlation, where higher interest rates are matched with higher home prices.

Basically, looking at mortgage rates as a factor in determining home prices over the last three years has been confusing, at best. But the Bank of Canada and other Canadian agencies have decided that interest rates are an effective tool to "steer" the home market anyway. Even the Trudeau's government thinks a first-time home buyer program that will offer a zero percent and principal-free loan will help boost home prices. It might, but according to the data, not because it's interest free.

How mortgages are significantly correlated with home prices

With the latest data on home prices from Stats Can showing quite the deterioration in growth, it's worth pointing out that there's actually a correlation between residential bank mortgage credit and home prices. Below is a chart that uses Statistics Canada's national home price index and total national residential mortgages issued by the commercial banks.

Canadian Residential Bank Mortgages and Canadian National Home Price Index (Stats Can) - June 2016 to June 2019 (monthly)

Source: Fertsman.com | Statistics Canada

An r-squared value of 0.92 is a much more robust figure than the one we got for interest rates. Here, we can see how the quantity of mortgage credit measured in Canadian dollars is positively correlated with home price growth. Bank mortgage credit statistics explain growth to a statistically significant degree.

The thing that I hope you take away with you after reading (or listening to this article) is that interest rates don't steer home prices, bank credit quantity does.